Meeting of Tax Administrators: Challenges and Opportunities (IV) Of Institutional Management

Does a tax administrator spend a large part of their working day on institutional management? The answer is undoubtedly yes. Anyone in charge of a tax administration has to plan, execute, and control personnel, purchasing, and financial and budgetary policies. These tasks take up a large part of their working day, and the assessment of their management will depend, to a large extent, on how they improve the organization by making appropriate use of all these elements.

If we agree that institutional management includes the policies, strategies and mechanisms used to organize the human, financial and material resources of a Tax Administration, we realize that the vast majority of actions conducted on a day-to-day basis have to do with all these issues, directly or indirectly.

About 60 experts from different international organizations in the tax world, such as the World Bank (WB), the Inter-American Development Bank (IDB), the Institute of Fiscal Studies (IEF) and the Inter-American Center of Tax Administrations (CIAT), participated in the meeting of Tax Administrators that was held in October 2025, at the Center for Spanish Cooperation in Montevideo (AECID). In addition, more than 20 Tax Administrations from America, Africa and Europe were represented. For 3 days, the challenges and opportunities related to 5 core elements or axes were discussed, including the institutional management of Tax Administrations.

Given the profile of the participants, it was possible to combine the broadest and most horizontal vision available to representatives of International Institutions and the practical, day-to-day experience of the top managers of the Tax Administrations represented at the event.

As a promoter of the event of this axis, of institutional management, in the three days of the event, I have to express my satisfaction for the ideas that, spontaneously, all the participants contributed in the proposed practice. As always happens in the events organized by CIAT, the atmosphere was fantastic and that, in my opinion, allowed the participants to express themselves with sincerity and honesty. As you can guess, it is difficult to be able to gather 60 top-level people and be able to spend 3 days thinking about possible challenges and opportunities of a Tax Administration. It is obviously easier for experts to participate in workshops, conferences and international meetings organized in round table formats, interviews, or individual presentations.

On the other hand, as you can guess, institutional management has a lot to do with all the other axes/components that were analyzed at the First meeting of Tax Administrators (human resources, technology, risk management and tax system), so some challenges and opportunities also appear in other components, which, in my opinion, means that there are issues of such magnitude that they are considered priorities. Let us analyze them from one perspective or another.

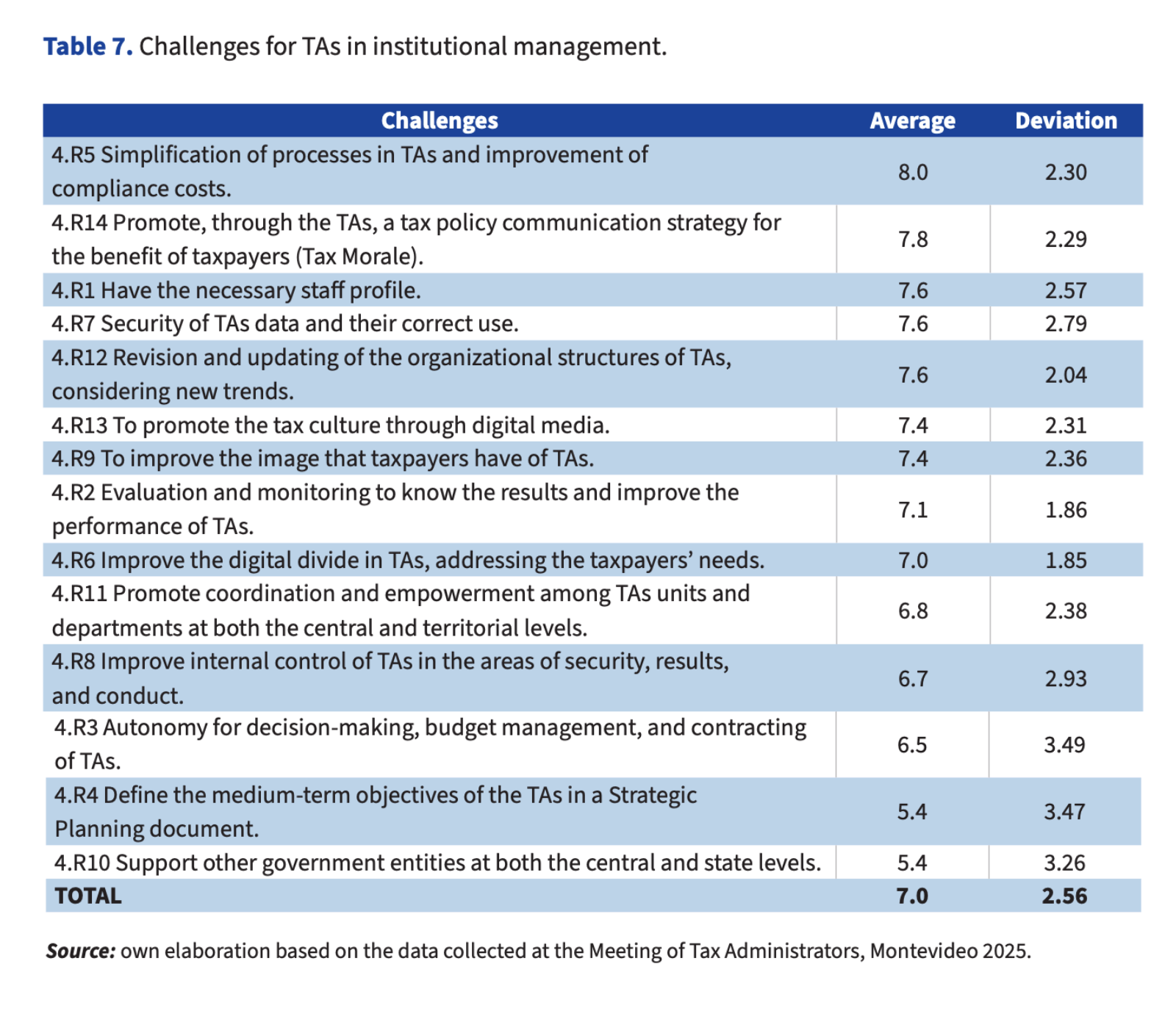

The challenges voted on the last day of the meeting, by the Tax Administrators in the institutional management component were, in order of score, the following:

As you can see in the attached table, 14 challenges were discussed by all the attendees at the meeting, with an average score of 7 out of 10 points and a standard deviation from the average of 2.56 points, which can be considered moderate-high.

Among the challenges that tax administrators highlight, we must mention, first of all, ”simplifying processes and improving compliance costs in tax administrations, with 8 points and that, in my opinion, is a permanent and fundamental objective of any Tax Administration that intends to provide a quality service to its citizens.

Secondly, the challenge highlighted by the tax administrators was to “promote a tax policy communication strategy from the tax administrations at the service of taxpayers,” with 7.8 points. It is necessary to make more efforts, on the part of the tax institutions, to communicate well and that the measures adopted are understood by the citizen-taxpayers. In my opinion, this idea combines elements that also have to do with transparency and the search for efficiency from the Tax Administrations. Coordination between institutions with competence in the field of fiscal policy and the implementation of that policy is therefore essential. As you know, in many countries they are different organizations.

Thirdly, tax administrators highlighted challenges such as “having the necessary staff profile,” “data security and correct use of data,” and “reviewing and updating organizational structures, taking into account new trends,” with a score of 7.6 points. This group of challenges includes personnel issues that are always the workhorse, and that involves finding and keeping the best, so that they provide a good service in tax administrations, more in very changing environments. Data security and its correct use is also a core element in any Tax Administration and requires a lot of human, technological, and financial resources. As for the need to have an organization adapted and designed according to the new trends, it is something that all tax administrations try to do in order to function efficiently, adapting, when necessary, their rules and seeking the autonomy that a good organization destined to collect a country’s taxes always requires.

Finally, among all the other challenges that were selected and that are also important, I want to make a brief comment about the importance of Tax Administrations in the lives of citizens and the need to support other government areas at times when it is essential, given the enormous amount of information available by tax institutions and the claim of these data in unforeseen situations and, in many cases, of extreme urgency (subsidy policy, attention to disadvantaged families, disaster situations, etc.). It is also advisable to strengthen the tax culture/morals of citizens and have the best possible Tax Administration, with means, management autonomy and placing the citizen-taxpayer at the center of its objectives.

In summary, the 14 challenges obtained an overall average score of 7.0 out of 10 (SD=2.56). The best rated was 4.R5 Simplification of processes in HTM and improvement of compliance costs (8,0), while 4.R4 Define the objectives of HTM in the medium term and 4.R10 Supporting other government entities obtained the lowest scores (5.4).

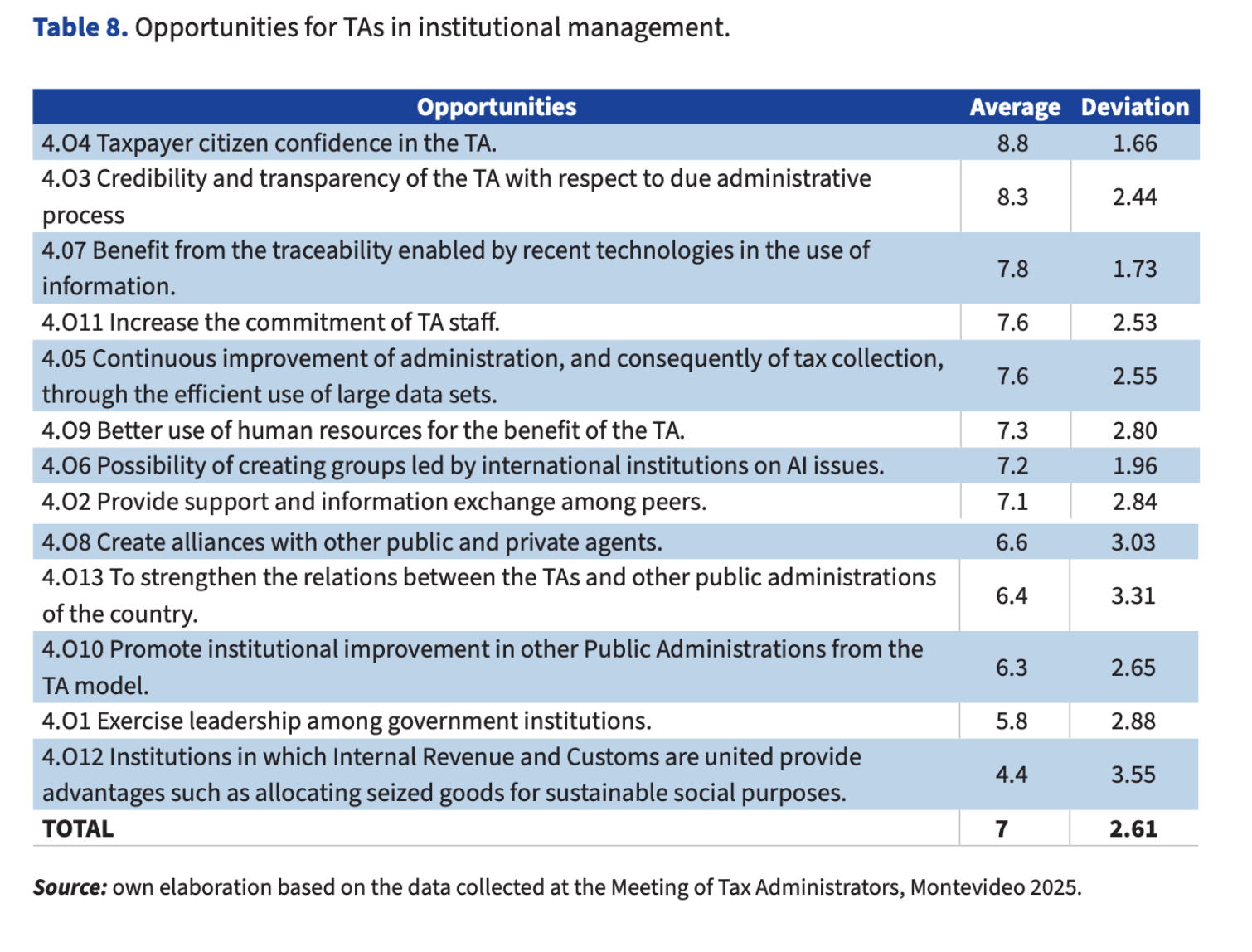

With regard to the opportunities or possibilities for improvement, starting from a certain situation, the tax administrators highlighted the following, in order of importance:

The average was again 7 out of 10 points, with a standard deviation from the moderate-high average of 2.61 points. The attendees of the event pointed out 13 opportunities regarding the institutional management axis/component.

In the first place, very prominently, “the confidence of the citizen-taxpayer in the tax administration” was placed as an opportunity, with an average of 8.8 points and a dispersion of only 1,66 points. In my opinion, it is essential that tax authorities earn the trust of taxpayers and become one of the leading institutions in the country. This task is never-ending, and we must be careful not to damage our reputation in situations that may arise, given how difficult it would be to regain the prestige that we have worked so hard to achieve.

Secondly, also by an exceptionally large majority, tax administrators highlighted the opportunity for ”credibility and transparency in the processes of Tax Administrations”, with an average of 8.3 points. The elements that are incorporated on this occasion are related to the trust that we pointed out in the previous section and the need to do things with the knowledge of citizens. More and more, in all CIAT member countries, there is a tendency to introduce rules that strengthen transparency in administrative procedures.

Finally, among the other opportunities identified, some especially important elements are included relating to:

- • The importance of having highly trained personnel who contribute to the fulfillment of the organization’s objectives. In addition, a fundamental aspect that concerns all Tax Administrations, at present, is how to retain talent.

- • The availability of technological means that facilitate the work and allow to achieve higher levels of efficiency is something that all Tax Administrations demand from their Governments. As we all know, any modernization process inevitably involves heavy investments in technology.

- • Cooperation between Tax Administrations of different countries, sharing information and enabling the participation in joint audits. It is also necessary, from the tax organizations, to support and maintain good relations with other national institutions, supporting certain judicial, administrative, or other processes.

In summary, the 13 opportunities identified reflect an average rating of around 7 points. They clearly highlight the taxpayer-citizen’s trust in the TA (8.8) and credibility and transparency (8.3) as the best valued opportunities, which underlines that institutional legitimacy is perceived as the most valuable asset of Tax Administrations. It is followed by the use of new technologies and the traceability of information (7,8), as well as the commitment of staff and continuous improvement through the efficient use of data (7,6). At the lower end, the institutional leadership (5.8) and the advantages derived from the union of Internal Revenue and Customs (4.4) obtained less support.

In conclusion, the exercise held at the AECID headquarters in Montevideo, in October 2025, was fully successful and allowed CIAT to have first-level information on the challenges and opportunities in different areas of the Tax Administrations of its member countries. They will serve to provide support, in a focused way, in those most necessary areas of action. In this regard, I hope that the Second Meeting of Tax Administrators, to be held in Madrid at the end of September 2026, will attract as many experts as possible and that the working methods will once again be original and useful, enabling us to produce a new publication of interest to the tax community.

The document on the meeting, published by the CIAT Secretariat last January, provides detailed information on the averages and standard deviations of the fourteen challenges and thirteen opportunities for this axis/component, as identified and assessed during the Montevideo meeting. Go ahead, download it and study it… here is the link

Kind regards

2,472 total views, 2 views today