Meeting of Tax Administrators: Challenges and Opportunities (III) – Risk Management

In October 2025, under the auspices of the Spanish Cooperation, the DGI of Uruguay and CIAT, an innovative exercise, articulated through a carousel methodology, took place in Montevideo. This dynamic has allowed us to get to know first-hand the challenges and opportunities of tax administrations of CIAT member countries from America, Africa, and Europe, in various fields of action: Human Resources, Technology, Risk Management, Institutional Management and Tax System. These challenges and opportunities were identified and put to a vote by the representatives of the tax administrations (TAs) present, which has allowed evaluating the specific weight of each of them and the level of consensus among the participants. Representatives of the IMF, the BI, the UNDP, and the IEF of Spain also participated in this exercise.

In this blog, I will share with you some thoughts regarding the adoption of a Risk-Based Management Approach (RBA), based on international trends and the results of the Montevideo meeting.

Personalities from the business world have stated, in different ways, that successful companies are those that effectively manage risk and make long-term decisions. This also applies to the tax administration, which exercises a dual role of ”facilitation“ and ”compliance control.” An RBA helps to make informed decisions and contribute to short, medium, and long-term planning, facilitating the sustainability of the ”business” over time.

Thanks to the work of international organizations that have disseminated good practices and advantages of the RBA, tax administrators are more aware that managing risks involves a cultural transformation. Gradually, the traditional and limited view that risk management consists only of identifying non-compliance in order to take repressive actions has been abandoned.

Adopting an RBA implies a radical change in the actions of the TA, so that it provides each taxpayer with a treatment according to their behavior, preventing, in turn, the materialization of known risks. In this sense, it is necessary to have a comprehensive diagnosis of the tax system (e.g., rules, procedures, administrative and operational aspects) and to have a well-structured investment plan.

There are still few consolidated experiences of TAs that adopted an RBA. For example, in Latin America (LA) many TA have innovative procedures and technologies that allow managing risks. However, for most of them, the adoption of an integrated approach remains a pending issue. Internationally, the United Kingdom, Australia and Spain have made great progress on this approach. In LAC, Chile has been a pioneer. The Handbook on Non-Compliance Risk Management for TAs [1] presents in detail the main aspects that make up the construction of this approach, focusing on the experience of the TA of Chile.

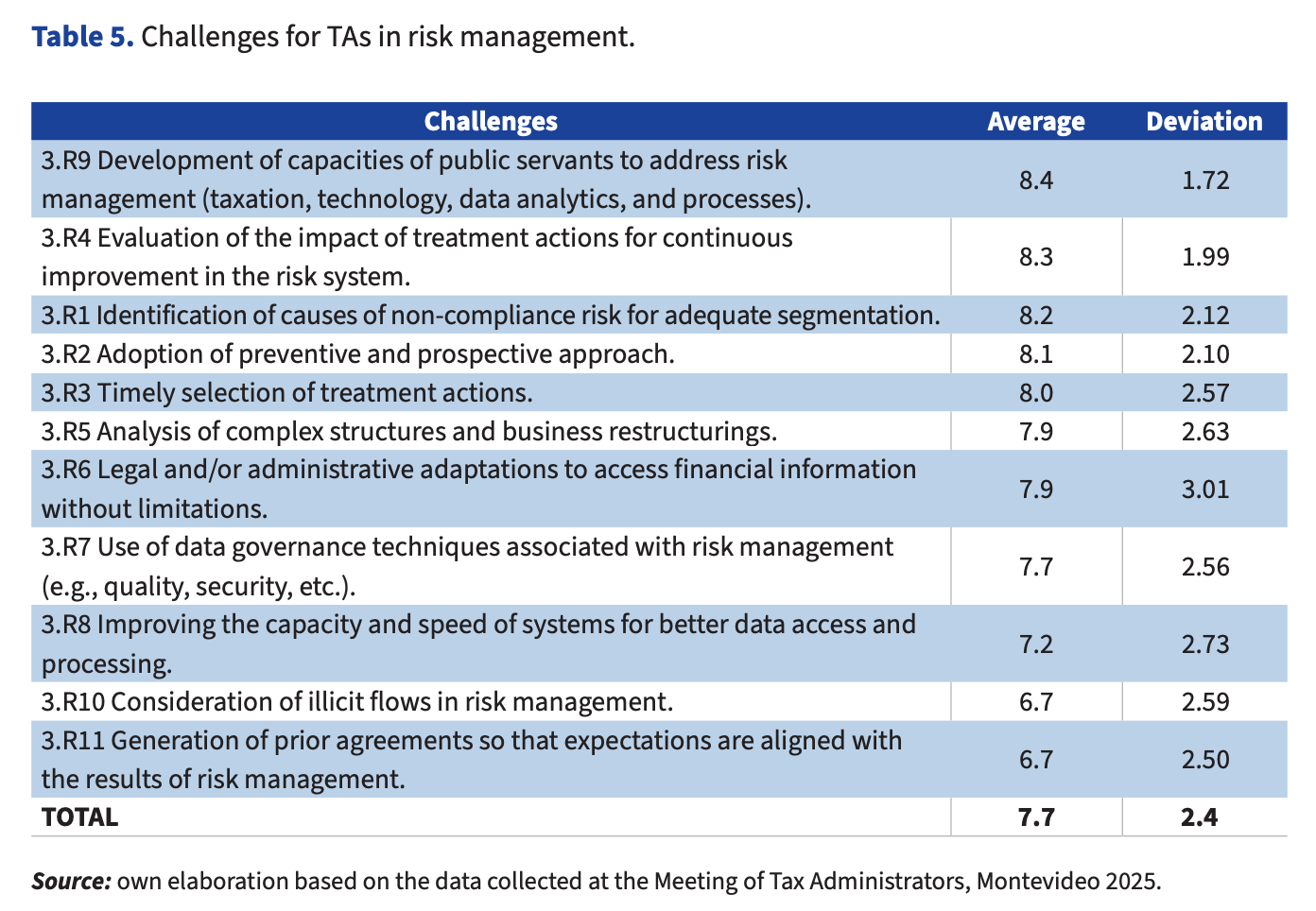

The document Opportunities and Challenges of TA (CIAT, 2026)[2], includes in its table 5 the main challenges identified and their order by valuation (total mean 7.7; deviation 2.4).

It can be seen from this table that, despite technological advances and forecasts about a lower dependence on personnel, as a result of the use of artificial intelligence, having adequate and sufficient human resources is the main challenge faced by tax administrators. In this sense, it is strategic for TAs to allocate more resources to staff development, especially in the areas of taxation, technology, data analytics, and process management. Personnel remains the main asset of TAs and one of the biggest concerns of tax administrators.

The second most outstanding aspect is related to the need to measure and analyze the impact of treatment actions. Measuring the impact of management provides critical information for proper planning and is a challenge for many TAs, which for various reasons do not have effective management measurement or monitoring tools.

The third challenge, in order of priority, is related to the identification of the causes of the risk of non-compliance. This work, like the measurement of the impact of management, is part of the systematic risk management process. Understanding the causes of non-compliance allows a better segmentation of risks, knowing their potential impact, designing, and adopting more effective actions.

The following eight challenges are no less important. For example, adopting a predictive and prospective approach is a task that involves gradual development and depends on the ability to timely access quality data and the intensive use of technologies. Adopting a preventive and prospective approach in the complete cycle of the tax system can be considered as aspirational, even for the best TAs. However, there are numerous opportunities for a TA with a moderate degree of maturity to adopt it in specific cases (e.g.: provide timely information to the taxpayer, generate pre-prepared returns, analyze big data from electronic invoices, adopt advance information regimes, etc.). Challenge number 11 on the table (C11) ranks among the lowest in terms of priority (6.7 on average and a deviation of 2.50), but it is fully aligned with this approach, given the preventive impact of properly negotiated prior agreements.

The timely selection of treatment actions requires precise coordination between the area that analyzes risks and the one that selects or proposes them. It is not recommended that the unit that analyzes the risks is also the one that selects actions, since the latter complements its operational experience with conclusions based on documentary evidence. Here, the challenge is to generate mechanisms that promote good communication and feedback, facilitate continuous improvement in the identification of risks, and contribute to the definition of the menu of treatment actions and their appropriate selection.

A challenge that is closer to the total average (7.7), but which is no less relevant, given the impact that large companies represent on tax revenues in developing countries (especially in income tax), is that related to the analysis of complex structures and business restructuring. This work largely depends on the capacity of the human resources of the TA, the level of international/domestic cooperation and the regulatory framework for large companies (e.g.: information regimes, anti-abuse rules, etc.). In this regard, it is recommended to read the following documents: The Trust and other complex structures (CIAT, Latindadd, NORAD, 2023) and the Manual on the Control of Aggressive International Tax Planning (CIAT, GIZ, EUROsociAL+, 2022).

The R10 is in the penultimate place, perhaps because it does not aim at the main objective of the TA. However, it reflects an extremely important aspect, which is the ability to detect and report illicit financial flows. This work is closely related to the control of large companies, international operations, high income/wealth individuals, and complex structures.

Two especially important challenges, which are ranked around the overall average and one step below it, are R7, referring to the use of data governance techniques, and R8, related to improving the capacity and speed of systems. It is essential to address these challenges in order to make the system work properly. The document entitled Data Governance for TAs (CIAT, 2024) provides details on the challenges and opportunities associated with this issue.

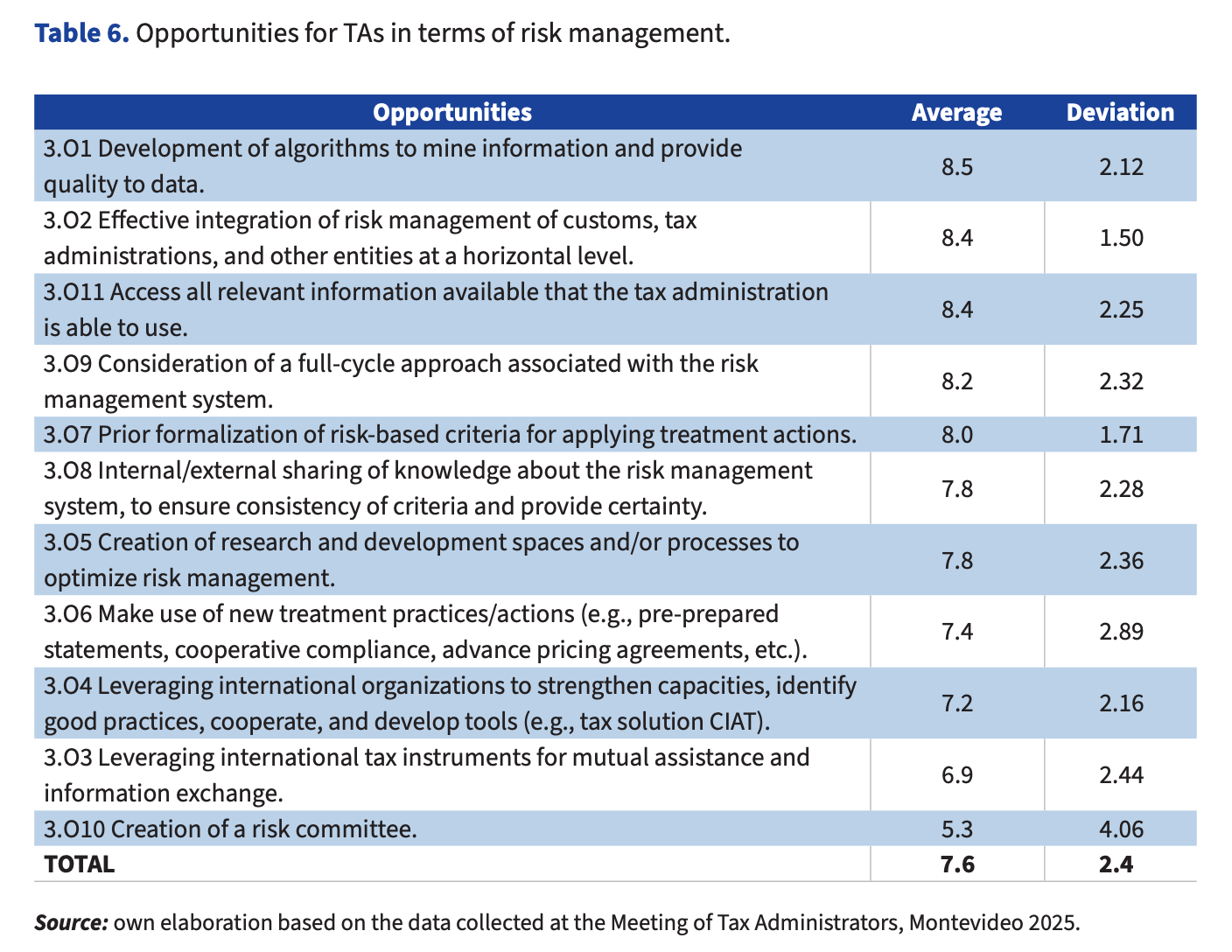

As for the opportunities in terms of risk management, Table 6 of the aforementioned CIAT document shows the conclusions obtained, with the total average being 7.6 and the deviation being 2.4.

The vast majority of tax administrators present in Montevideo (average of 8.5 and deviation of 2.12) considered that data quality is essential to address adequate risk management, raising the opportunity to use algorithms to provide data quality and mine information. In doing so, they acknowledged that the cross-referencing of information traditionally conducted by tax authorities is insufficient, and that it is necessary to develop algorithms that take more variables into account and enable sophisticated analysis.

The second most relevant opportunity (average of 8.4) is to adopt an RBA at a horizontal level (e.g., taxes, customs, social security resources, and others). There is a higher level of consensus about this opportunity than in the O1 (deviation of 1.5). This integration or coordination allows generating synergies between public agencies and adopting a single state vision, maximizing access to information and consequently efficiency. However, this requires the creation of effective communication channels, the harmonization of capabilities, and the overcoming of regulatory constraints (e.g., secrecy). In the same order of priority (8.4 on average) but with lower consensus (deviation of 2.25), the tax administrators highlighted the opportunity to work on greater integration within the TA itself, accessing all the relevant available information that it is able to take advantage of. In this way, it is considered that the limit on access to information should be marked by processing capacity, thus avoiding the establishment of information regimes that cannot be processed.

The full-cycle view is fundamental to anticipating consequences of actions in different instances (e.g.: control and collection) and has been considered as an opportunity by a significant proportion of tax administrators.

With the aim of making decisions based on evidence, following predefined and harmonized criteria, the tax administrators considered it appropriate to formalize risk-based criteria in advance to apply treatment actions. On this aspect, the average was 8.0 and the deviation was 1.71.

Two opportunities that were valued in similar proportions (average of 7.8) and with a similar level of consensus (deviations of 2.28 and 2.36) were the internal/external socialization of knowledge about the risk management system and the creation of spaces and/ or research and development processes. Both aspects are fundamental to ensure that a TA is consistent in the application of criteria and provides sufficient certainty to taxpayers.

The creation of a research and development (R&D) unit or function is perhaps one of the greatest opportunities for TAs, given that it is difficult to innovate when all their staff participate in operational or routine tasks. This space allows to study, develop and evaluate their own or existing good practices, without significantly interfering with the operational capacity of the institution and allowing to adopt a continuous improvement approach. It is no coincidence that R&D is a critical area for companies.

To a lesser extent and with a lower level of consensus, four truly relevant practices were identified as opportunities. The first is related to the increase of the “menu” of treatment actions, based on good international practices. A menu with more actions would allow a better personalization of the care or treatment that TA’s provide to taxpayers. Linked to this issue, the opportunity to go to international organizations to identify good practices, learn how they work, implement them, and develop solutions has also been highlighted. In this regard, CIAT makes available to its members the Consultation Service and the Tax Help Desk, the Maturity Model on Dispute Prevention and Resolution, databases on various tax matters and the documents of its library. ISORA is also a useful tool for this purpose. In terms of IT solutions, CIAT offers the DEC system (tax management for the sale of digital goods and services) and the Electronic Invoicing Anomaly Detector (e-IAD).

Another aspect discussed relates to international tax cooperation in administrative matters, which is still underutilized by many countries, especially with regard to the effective use of automatic exchange of information, joint, simultaneous, or external audits and collection assistance.

The creation of a Risk Committee is a practice that has worked in several countries and that facilitates, among others, the construction of the risk catalog, the prioritization of risks and the approval of compliance strategies: ensuring the participation of critical areas and defining harmonized criteria. This opportunity has been the least voted (average of 5.3 and deviation of 4.06) but is worth noting.

The adoption of an RBA requires, at least, the following critical elements: sufficient and suitable human resources in multiple areas of knowledge, a change in the institutional culture, an adequate balance between evidence and expert judgment, effective coordination and cooperation, both internal and external, a lot of institutional discipline, and a thorough and rigorous planning. In this context, technology is the support that allows all these elements to be articulated and enhanced.

The activity in Montevideo has allowed us to know the interest and priorities of TAs in this vast and complex matter and left us with ideas on aspects that deserve to be discussed in greater depth and that we hope to deal with in future CIAT activities.

References:

[1] The Manual on Non-Compliance Risk Management for Tax Administrations. CIAT, SII of Chile, SAT of Mexico, GIZ, IMF and IDB, 2020.

[2] Opportunities and Challenges of Tax Administrations. CIAT Tax Administrators Meeting 2025 2026, CIAT.

2,204 total views, 2 views today