Tax Treaties in Latin America

Some statistics from CIATData

As we do on a regular basis, we have just updated the information on Double Taxation Avoidance Agreements (DTAs) and on Tax Information Exchange Agreements (TIEAs) signed by CIAT member countries in Latin America. This time, the update was until October 31. Not only the update but the information has been improved with data on treaties that are no longer applied and those that were renegotiated.

As we do on a regular basis, we have just updated the information on Double Taxation Avoidance Agreements (DTAs) and on Tax Information Exchange Agreements (TIEAs) signed by CIAT member countries in Latin America. This time, the update was until October 31. Not only the update but the information has been improved with data on treaties that are no longer applied and those that were renegotiated.

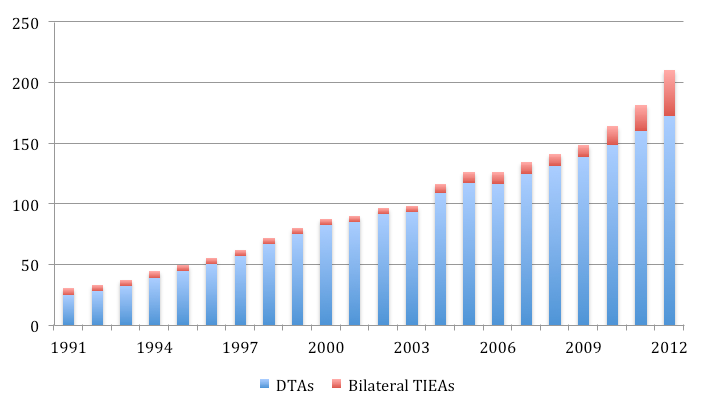

A total of 172 DTAs are being applied in the countries of the region. The panorama is known. The countries showing the largest networks of agreements are Argentina (16) Brazil (31), Chile (24), Ecuador (12), Mexico (42) and Venezuela (31), although from Argentina and Ecuador nothing new has been reported since 2002 and 2005, respectively, and it is known that the former has denounced two (2) recently. Another country with a remarkable network is Bolivia (7), although nothing new has been reported. The Central American countries (and the Dominican Republic) are those who have the least opted for these instruments.

Nevertheless, it is interesting to see what other countries have been doing in recent years. The case of Panama is the most striking. From not having any DTA in 2010, it will have 10 in 2013. Another country of similar size is showing a similar behavior: Uruguay. With presently only one DTA in force, they will have 7 in 2013. Finally, Colombia, which in 2004 only showed the Decision 578 of the Andean Community, will have five DTAs enforced in 2013. Additionally in all these countries there are other treaties in process of ratification in Congress, so that even more results can be expected.

On a lesser note, Peru and Paraguay have also shown an increased activity. Peru has a very limited network of DTAs, despite being a country with great economic potential in the region. Until 2004 only 3 were in force, including Andean Community Decision 578. One was added in 2010 and 4 additional ones are in the process of ratification by Congress. Paraguay gave signals only in 2009 and 2010 when their first 2 CDIs entered in force. After that they showed no activity.

On the other hand, the new CIATData information also shows the evolution of cooperation and mutual assistance policies in preventing international tax evasion. Even though DTAs contain clauses in this regard (Article 26, Article 27 of the OECD and United Nations Model Convention), several countries in the region have preferred to enter into bilateral TIEAs instead of DTAs so as not to limit their power as source countries for taxing the income generated within their jurisdiction, or adhering to multilateral mutual administrative assistance efforts

There are 38 bilateral TIEAs in force in Latin American countries –including those signed under the CIAT Model Agreement and Memoranda of Understanding– although these are strictly concentrated in only three (3) countries: Argentina (12), Costa Rica (6) and Mexico (12). Virtually all the TIEAs entered in force after the recent financial crisis. There is no doubt that the political momentum impulse by the G20 countries to tax information exchange for reducing the fiscal deficits increased the signing of these agreements worldwide.

On the other hand, the Global Forum on Transparency and Exchange of Information has contributed to promote the effective implementation of the international tax transparency standard. We already have mentioned Costa Rica, where in addition to the agreements in force, there are 9 additional agreements in process of ratification in Congress. Likewise, although Guatemala and Uruguay still have no agreement in force, they have signed 7 and 9 bilateral agreements respectively, which are now in process of ratification by Congress.

Finally, it should be noted that countries of the region that have signed the Multilateral Convention on Mutual Administrative Assistance in Tax Matters are Argentina, Brazil, Colombia, Costa Rica and Mexico. It should not be forgotten that the Central American countries maintain a Multilateral Convention on Mutual Assistance and Technical Cooperation between Tax and Customs Administrations which, although still awaiting ratification in some countries, involves other multilateral cooperation efforts.

DTAs and TIEAs being applied in Latin America

(Updated through October 31, 2012)

17,635 total views, 12 views today