Potential effects of a carbon tax on GDP in Latin American countries

Summary, by Andre Dumoulin of the study of Luis Miguel Galindo Allan Beltrán Jimmy Ferrer Carbonell José Eduardo Alatorre, ECLAC

The carbon tax and the environmental tax reform

Global studies on carbon taxation attempts at measuring potential effects on environment, economy and health; the present ECLAC study[1] focus on presenting the potential effects on GDPs in Latin America. It is noteworthy that in most cases, the collected data present a beneficial effect.

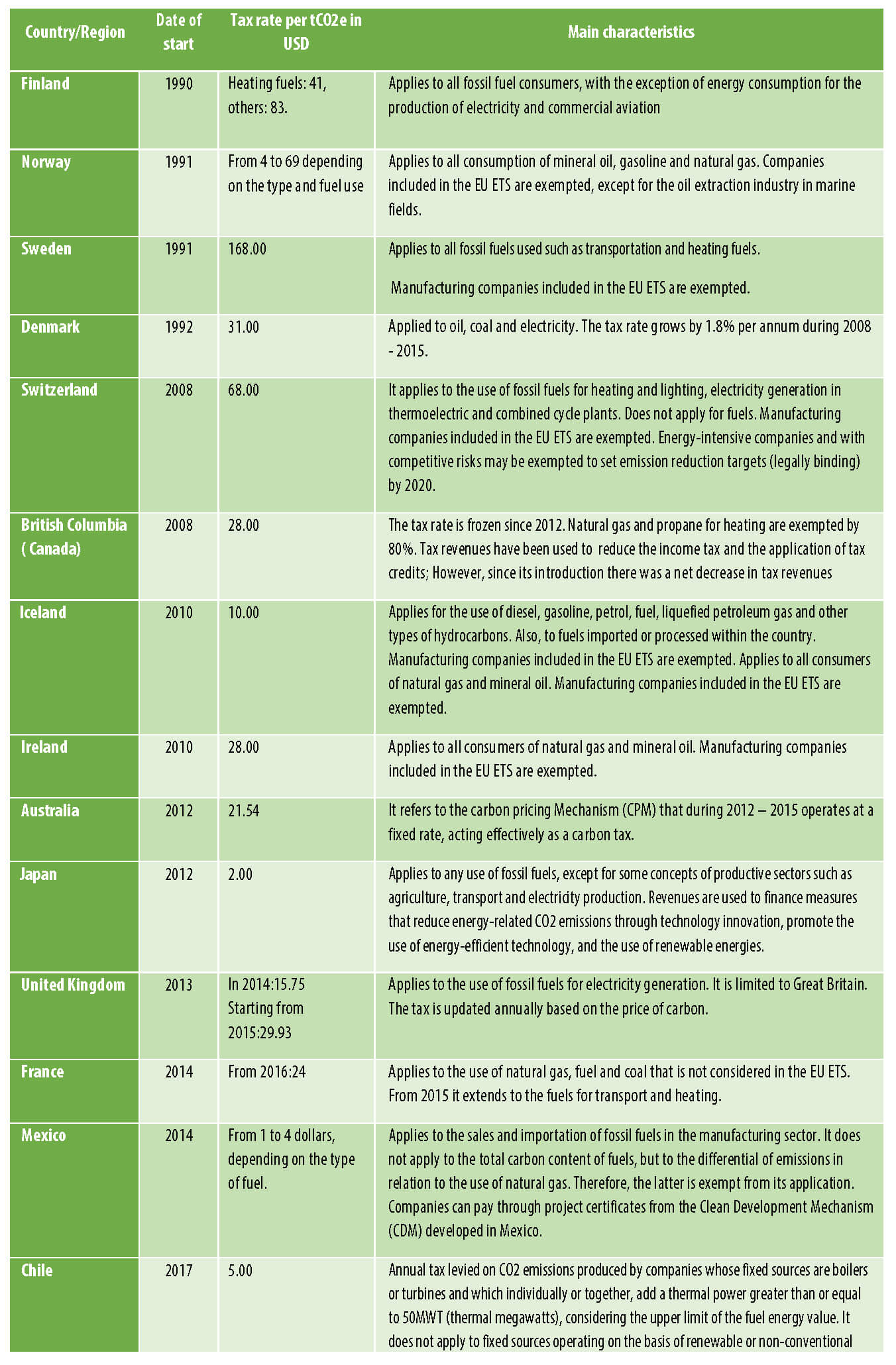

Environmental tax Reform (RFA) is defined as a reform of the national and international tax system reflecting a change in the tax burden from conventional taxes, such as those on labour or capital, towards taxes on activities that harm the Environment (EEA, 2005). In this way, a RFA should be understood as a change in the taxation structure, and not as an increase in taxation. Green or environmental fiscal reforms, instrumented during the 1990s, became a tool in international environmental policies and where carbon taxation has become an important element in particular in developed countries (JOFRA and Puig, 2014; CEFP, 2015). For example, Finland introduced a carbon tax since 1990; later (1991 – 1992) this tax was introduced in Norway, Sweden and Denmark. In addition, since 2008, it is applied in Switzerland and in the province of British Columbia, Canada. It is currently used in a large number of countries in Europe, as well as in Chile, Mexico, Japan, Australia and South Africa (from 2016). Let us remind that carbon taxes supplement or replace emission-trading schemes (ETS).

The following table provides a summary of the international experience of direct carbon taxes, including the tax rate established in each country, as well as its main characteristics. Currently, about 40 countries and more than 20 sub-national governments (cities, States or regions) have implemented some kind of carbon pricing mechanism including taxes, emission trading schemes, bonds, among others. Together, the instruments cover about 7 gigatons (Gt) of CO2, that is to say, about 12% of global emissions and at least 14 countries already have a tax in force.

International experience in the application of carbon taxes

In general, it is observed that in European countries, direct carbon taxes consider a proportion of their total GHG emissions (between 15 and 50%), in addition, those sectors that already pay a price within the emission trading system of the European Union (EU ETS) are exempted, thus avoiding double taxation. In general, higher taxes are applied in European countries, specifically in northern Europe. Sweden is the country with the highest tax, amounting to $168 per tCO2e, followed by Switzerland and Finland with a rate of over $60. On the other hand, in countries like Iceland, Mexico and Japan, the tax is lower with rates below 10 dollars. In addition, it is observed that more and more countries, especially those of the OECD, have incorporated the carbon tax. However, the experience in the use for Latin America and the Caribbean (LAC) still scarce except for Mexico and Chile, and lately Colombia has introduced a similar tax.

The authors have completed a meta-analysis and a statistical meta-regression based on 35 studies on the macroeconomic effects of a carbon tax based on computable General equilibrium models published between 1992 and 2015.

Estimated impact of a carbon tax on GDP (in the long term)

The results suggest that the application of a carbon tax for Latin American countries could have positive impacts on GDP as they would generate incentives for the implementation of new technologies, more energy efficient and would generate incentives for the development of other economic sectors less intensive in the use of energy.

Income-reuse schemes that consider reducing capital and labour taxes contribute significantly to lower the economic cost of implementing a carbon tax. For this reason, the transfer of coefficients for Latin American countries considers three scenarios on the re-use of taxes.

ms_list item_border=”no” item_size=”14″ class=”” id=””]

According to the results, the two scenarios of reusing the income result in a decrease in the macroeconomic cost associated with the tax.

The results suggest that substituting taxes on the productive factors with environmental taxes results in a net economic benefit for assessments of up to $75/tCO2e, depending on the country. However, the marginal benefits of this substitution are declining, so passing the optimal level of tax suggested for each country, the benefits of reducing taxes on productive factors are lower than the additional distortions caused in the economy by higher levels of a carbon tax. Thus, although higher levels of taxation would result in an environmental benefit, the economic benefits would decline to become negative in most countries and for tax levels exceeding $75/TCO2.

In the results, it is appreciated that the tax revenue reuse schemes allow reducing the economic costs of the implementation of the tax on CO2 and even to obtain a double dividend. In this way, the reuse of income allows raising the optimal level of carbon tax in the countries of the region, thus in addition to the environmental benefit derived from the reduction in CO2 emissions, the re-use of the income would result in greater economic benefits that would range between 0.01 – 8.26% of GDP depending on the country and the reutilization scheme considered. The foregoing implies that there would be benefits of implementing environmental tax reform with a focus on fiscal neutrality and on partially substituting taxes on productive factors with environmental taxes or social security contributions.

[1] See document (in Spanish): http://repositorio.cepal.org/bitstream/handle/11362/41867/1/S1700590_es.pdf

3,741 total views, 2 views today