E-tax invoicing and virtual services support the business continuity in Brazil during the COVID-19 pandemic

For some time now, the tax administrations of Brazilian states have been modernizing to offer virtual services to taxpayers in order to improve the functioning of the economy and the fulfillment of various tax obligations. As a result, the need to move personally to the federal tax offices or state and municipal treasury departments has been reduced, making life easier for taxpayers. These virtual services become more important due to the advance of the coronavirus pandemic (COVID-19), which leads to reduce the movement of people and increases the importance of the telework.

The virtualization of tax services implies a paradigm shift. Part of this change is the electronic tax documents available exclusively through the internet, such as the electronic Tax Invoice (Nota fiscale elettronica-NF-e), The Electronic Consumer Tax Invoice (Nota fiscale De Consumidor elettronica – NFC-E), and the public Digital Accounting System (Sistema Público de Escribturação Digital – SPED). These electronic documents allow the virtual sending of all tax and accounting information from companies to the tax authorities. By completely eliminating the need to process or archive physical documents and by instituting a set of documents whose existence is exclusively electronic, tax processes become more agile and reliable, transforming the relationship between the tax collector and the taxpayer. This change was made possible by national regulations that gave the digital signature a guarantee of authenticity and integrity, as well as to documents in electronic format.

The digital transformation of the Brazilian tax systems was driven by tax administration modernization programs such as PROFISCO, promoted by the Inter-American Development Bank (IDB). This program enabled Brazilian states to make significant investments in areas such as process review, the development of more modern and Integrated Information Systems, the use of new technologies such as artificial intelligence, the improvement of technological infrastructure, and the implementation of solutions for computer security.

What is the importance of electronic tax documents for the tax administrations at this time of crisis?

Imagine how the monitoring and forecasting of revenue was carried out a few years ago. In the 2008 economic crisis, tax auditors had to answer frequently asked questions from state secretaries of finance about future revenue performance. They consulted directly with representatives of key sectors to obtain up-to-date sales information and thus update their projections. It was like a handcrafted work and, often, inconsistent over time. Let us also imagine how fiscal control would have been carried out if, in that crisis, telework had been compulsory. Tax administrations were certainly not prepared for this challenge as they depended, to a large extent, on paper documents and on on-site auditing.

The current health crisis came at a time when the tax authorities already have electronic tax documents, information on the taxpayer’s operations, and tax monitoring and control systems. These instruments make it possible, on the one hand, to forecast revenue, based on data from operations carried out in real time and, on the other hand, to increase the control of possible deviations.

It is clear that the factor that most impacts the collection is the economic activity, strongly affected by the pandemic. However, electronic tax documents and automated systems minimize the impact of the crisis on revenue by enabling the functioning of tax systems, even when the work is done remotely.

The benefits of electronic tax data

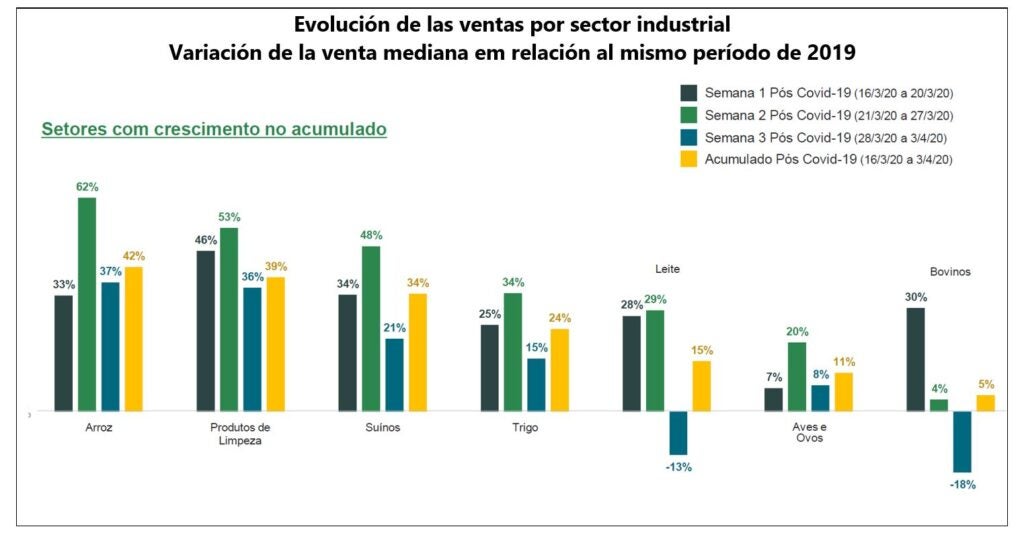

Advances in the production of tax data have also enabled state finance secretariats to produce studies and bulletins on the impact of the pandemic on the economies of the states. From the daily analysis of the electronic tax invoices issued and their comparison with the same period of the previous fiscal year, it is possible to identify what are the main sectors and municipalities affected by the crisis. This type of analysis is important for the tax authorities, as it allows for more accurate forecasting of revenue; at the same time, it allows other government bodies to formulate public policies to mitigate the effects of the crisis. They also reveal to the markets which are the most affected sectors and economic trends; and finally, citizens are allowed to follow changes in prices, mainly of products related to public health, something we have explored in a recent blog on collecting welfare.

In the graphs below we present some examples taken from the bulletins of the states of Rio Grande del Sur and Pernambuco, using the electronic invoice to monitor the behavior of markets and economic activity in general:

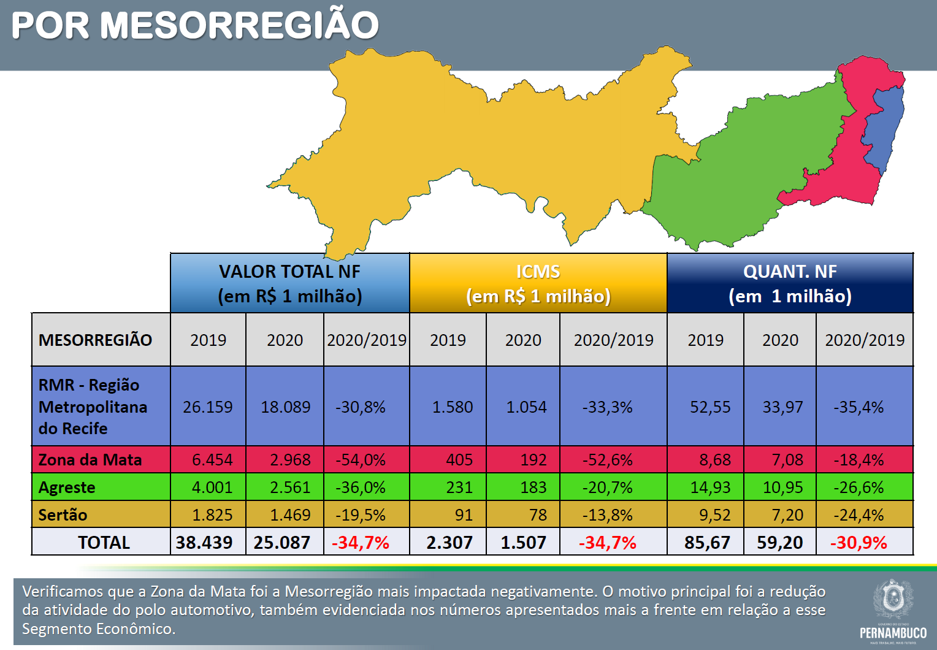

This graph shows the impact of the pandemic by region on the economies of Brazil’s States. From the daily analysis of the electronic tax invoices issued, and their comparison with the same period of the previous fiscal year, it is possible to identify the regions most affected by the crisis.

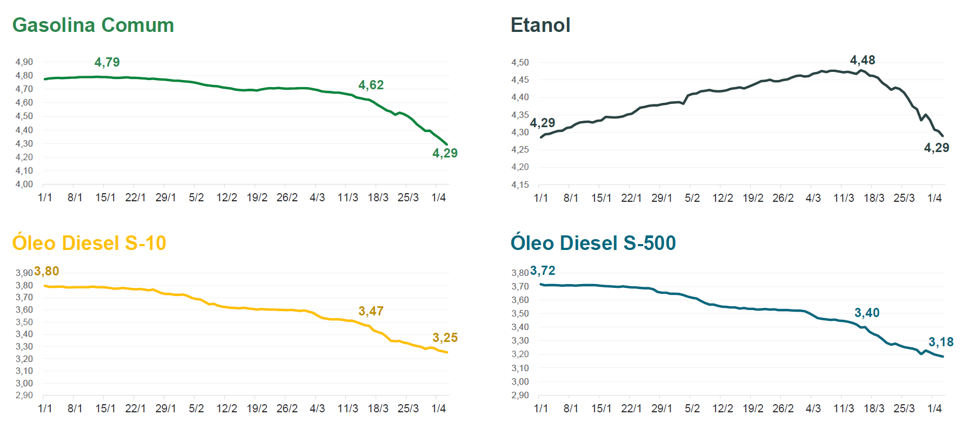

Examples of monitoring the fuel prices evolution.

Imagine now the paper tax invoices authorized in the farm units at a time when internet sales (e-commerce) became essential due to the isolation caused by the health crisis.

The implementation of the electronic tax invoice generated significant changes in the logistics chain between companies, distributors, and carriers, as it is issued in real time and simultaneously links all actors. In practice, the electronic tax invoice became the axis between the different stages from the purchase to the delivery of the product to the final consumer. It is this technological transformation that has allowed e-commerce to work smoothly, even in this context in which the on-site units of the tax administration are closed.

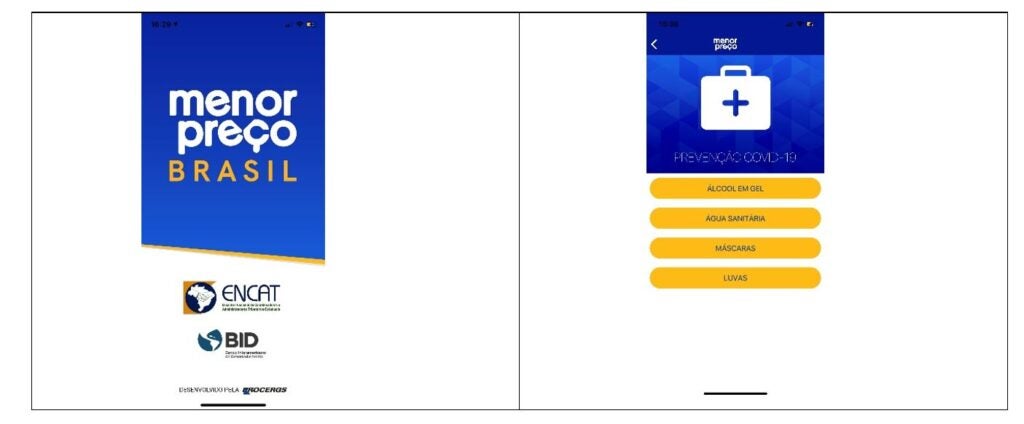

Data from electronic tax invoices and consumer notes are also feeding into the application database (app), “Lowest price Brazil” developed by the Ministry of Finance of the state of Rio Grande do Sul with the support of the IDB and the National Meeting of tax coordinators and administrators (Encontro Nacional dos Coordenadores e Administradores Tributários -ENCAT). This multifunctional app allows citizens to carry out inquiries of the current prices per product in the establishments of the selected region, indicating the date and time of the last purchases made.

Screenshot of the “lowest price app” developed by the Finance Ministry of the state of Rio Grande do Sul.

Screenshot of the “lowest price app” developed by the Finance Ministry of the state of Rio Grande do Sul.

In addition to the electronic tax invoice, there are many services provided by tax administrations that are necessary for the maintenance of the companies’ operations. The import of inputs and equipment for the health sector, for example, requires a payment and the entry clearance by the national and state tax administrations; the participation in bidding processes and the obtaining of bank loans, requires the presentation of the certification of absence of tax debts; the closing of a company, because of the recession triggered by the crisis, requires the tax registry de-registration request to be able to stop paying taxes.

Business continuity in electronic form

Currently, the services available on the internet for taxpayers allow their activities to continue, despite the fact that the vast majority of government bodies operate on a virtual basis. The single SISCOMEX portal, for example, allows import and export operations to be recorded, tax collection to be carried out, and the process to be accompanied and released, all without physical presence.

Also, Certificates of tax debt (Certificdão De Debitos Tributários – CDT) can be generated on the internet and have a guarantee of secrecy and security, as well as a validation code. All this allows the taxpayer to check his tax situation without the need to present physical documents or authenticate the signature of the competent authority.

For any alteration to the cadastre, such as the opening, modification and closure of companies, is available the National Network for Simplification of Registry and Legalization of Businesses (REDESIM), which enables the integration, in real time, of all the organs and entities responsible for the various administrative processes. Among them are the commercial boards, the bidding bodies, the Federal Revenue (Receita Federal), which is the tax body at the federal level, and the state and municipal treasury departments. This allows a single registration of information and documents exclusively via the internet, simplifying procedures and reducing processing times and bureaucracy.

In addition, if there is any doubt or question, taxpayer search and referral services, such as “talk to us” (fale conosco), messages and chats, are available on the electronic sites and ensure the resolution of problems and the maintenance of the relationship between the IRS and the taxpayer.

Extraordinary measures during the pandemic

Finally, it is worth noting that, due to the current crisis caused by the pandemic, the vast majority of Brazilian tax administrations, at the various levels of government, extended the deadlines for payment of taxes, quotas, and the delivery of ancillary obligations, and even the validity of the DTCs and special regimes, with the intention of allowing all to adapt as easily as possible to this moment of isolation.

The increasing demands of society for digital services, associated with new technologies, demonstrate the importance of the investments made by states in the expansion and improvement of solutions for the automatization of processes. By making it easier for citizens and businesses to meet their tax obligations, these digital solutions enable states to continue to collect resources at this critical time and maintain the provision of essential services to the population, contributing to saving lives.

This article was reproduced with the authorization of the authors (Maria Cristina Mac Dowell Dourado de Azevedo, Ana Lucia Dezolt, Soraya Naffah Ferreira and Patricia Bakaj) originally published on the IDB blog.

4,844 total views, 3 views today