British Columbia’s

Example in effective carbon taxation.

Example in effective carbon taxation.

OECD’s 2015 economic surveys recommends to Latin American developing countries, among other, “to make tax policy more progressive, more efficient and greener”. One key aspect of Greening the tax system is “adjusting the tax rates of the fuels to reflect their environmental impact”.

The successful conclusion of the Paris Climate Change Summit (COP 21) this December 12, 2015, leads me to write the present blog entry on the concept of carbon tax.

A carbon tax is a tax levied on the carbon content of fuels. It is a form of pollution tax. Carbon taxes offer a potentially cost-effective means of reducing greenhouse gas emissions. They help to address the problem of emitters of greenhouse gases not facing the full social and environmental cost of their actions.

Since lower-income consumers spend a greater proportion of their income on energy-intensive goods and fuels, tax revenues from carbon taxation should be used in favor of low-income groups or redistributed to them, in order to avert a regressive effect. (1)

A carbon tax is an indirect tax (tax on transactions). It is a price instrument: It sets a price for carbon emissions (due to their negative externalities, i.e. their effects on parties not involved in the transaction). One century ago, Arthur Pigou(2) already proposed taxing the goods which cause negative externalities (carbon dioxide in this case)

To date WTO case law has not provided rulings on climate-related taxes. However, it is believed that “carbon footprint taxes could serve as unilateral carbon policies allowing governments to undertake meaningful unilateral action on climate change without sacrificing the competitiveness of domestic firms and without violating the rules of international trade laws”. (3)

If a country introduce a carbon tax while another does not, competitive loss may be offset by border tax adjustments, trade tariffs and trade bans. However it is much more effective to coordinate national policies as countries are doing it against harmful tax competition

There are various tax concepts introduced for climate change mitigation:

- Emission taxes: Tax for every ton of greenhouse gas released into the atmosphere

- Energy tax: charged directly on the energy commodities

- Fee and dividend tax (enforced in British Columbia) the money collected from the tax is returned or credited to all households and other taxpayers, taxing carbon emitters and rebating those that burn less carbon.

Since British Colombia is the only case of a “carbon –fee and dividend tax”, we propose to show here some graphics released by the Sightline Institute, an NGO based in Seattle, Washington, founded by Alan Durning. (4)

British Columbia’s carbon tax shift has been implemented since July 1, 2008, with an initial rate of $10 per ton CO2. It increased by $5 per ton each year through July 2012, topping at $30 per ton, and did not change since. The tax applies to almost all fossil fuels burned inside the province.

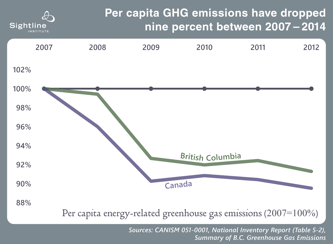

What happened to CO2 emissions in the province?

Emissions in BC dropped by 6% (and 9% per capita) between 2007 and 2011. During the same period, Canada’s energy-related emissions fell by an equal amount. In this regard, the influence of the carbon tax does not appear, because several other factors are interfering, such as the previous power plant structure.

By contrast, when we measure the Petroleum products consumption, here appear the best indicator of the influence of the tax shift on carbon pollution: The per-capita combustion of motor fuels decreased by 15% in the first four years of the tax shift, decreasing by 10 full points more than the whole of Canada.

A third consideration is that the carbon tax shift has not hurt the provincial economy: In terms of GDP per capita, the growth of British Colombia was a total of 6% between 2007 and 2013, the same as the whole of Canada.

Regarding inflation, prices in British Colombia have not diverged from those of the whole country during this period.

More important, the carbon tax shift has been revenue neutral: The following chart show how the carbon tax has been compensated by tax cuts: In practice, the tax shift has actually reduced tax revenue slightly overall, due to the decline in fuel consumption.

In this case, sightline.org states that the tax has become mildly regressive,

but an adjustment of tax cuts from business to low income households would make

the tax progressive again. The institute advocates for a return to a progressive growth of the carbon tax and adjustments to the compensating tax cuts.

Other carbon tax implemented in the world are in Australia ( $ 23 AUD per ton of emitted CO2, and the revenue raised was used to reduce income tax by increasing the tax-free threshold) Finland ( now $27 per metric ton) , Sweden, Norway, Denmark, the Netherlands. In these countries, however, business fuel use is taxed less than households fuel use.

Alan Durning concludes that the statutes and regulations used by British Colombia should be used and adapted in the tax codes of other states or province willing to implement a carbon tax.

2,340 total views, 3 views today