Meeting of Tax Administrators: Challenges and Opportunities (V) of the tax system

The final thematic session of the conference was held in October 2025 in Montevideo, sponsored by Spanish Cooperation, Uruguay’s DGI, and CIAT. It focused on the challenges and opportunities presented by the broader tax system – both national and international- in which tax administrations operate. While these factors generally fall outside their direct mandate—as they pertain more to tax policy—they significantly influence administrative activities.

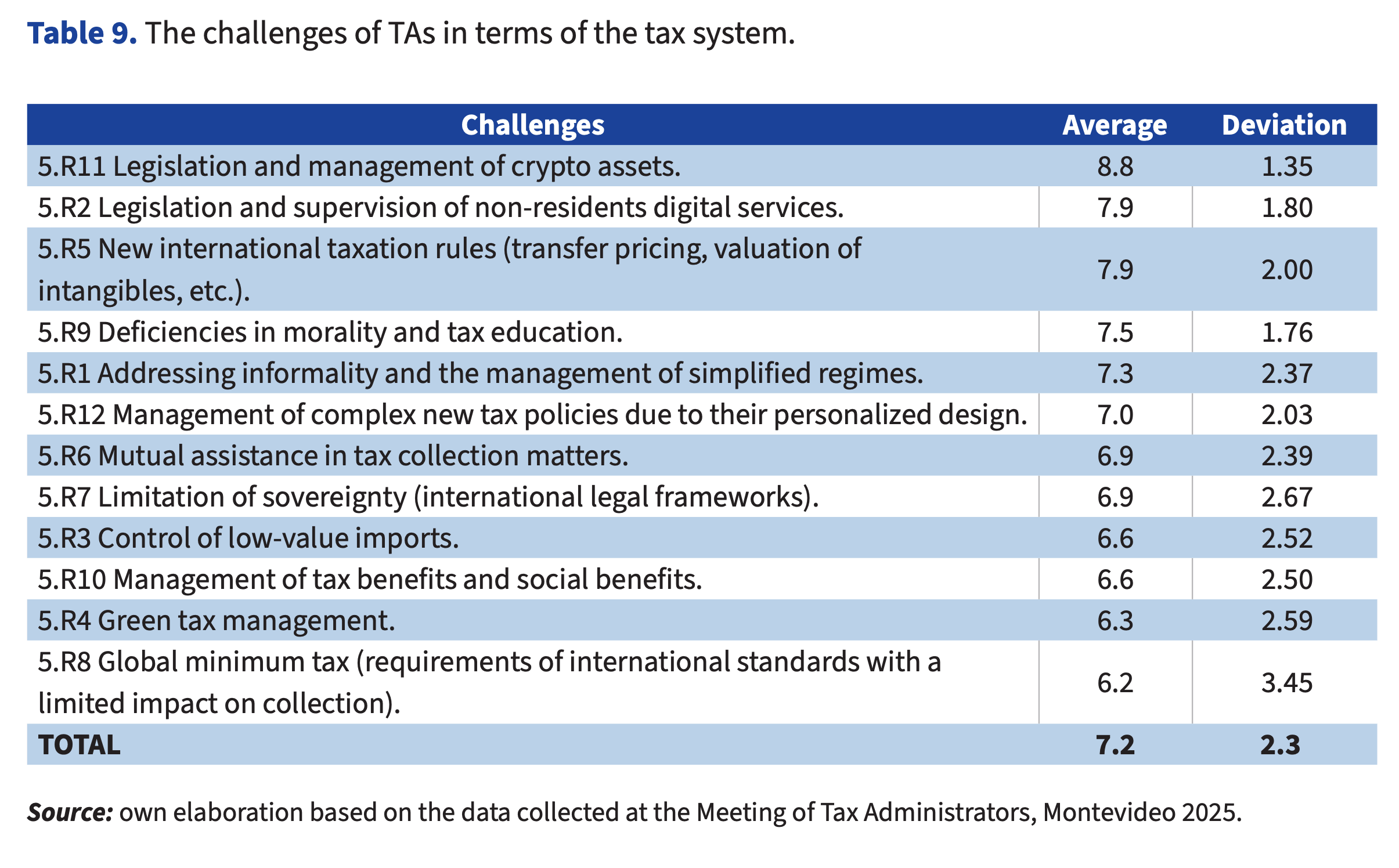

The most relevant challenges in this field are detailed in Table 9 (average 7.2; deviation 2.3) and ranked in the following order: legislation and management of crypto assets; legislation and supervision of digital services provided by non-residents; new international taxation rules; shortcomings in tax ethics and education; the informality and administration of simplified regimes; management of complex tax policies due to their tailored design; mutual assistance in tax collection; limitation on sovereignty (within international legal frameworks); oversight of low-value imports; management of tax and social benefits; management of environmental taxation; the global minimum tax.

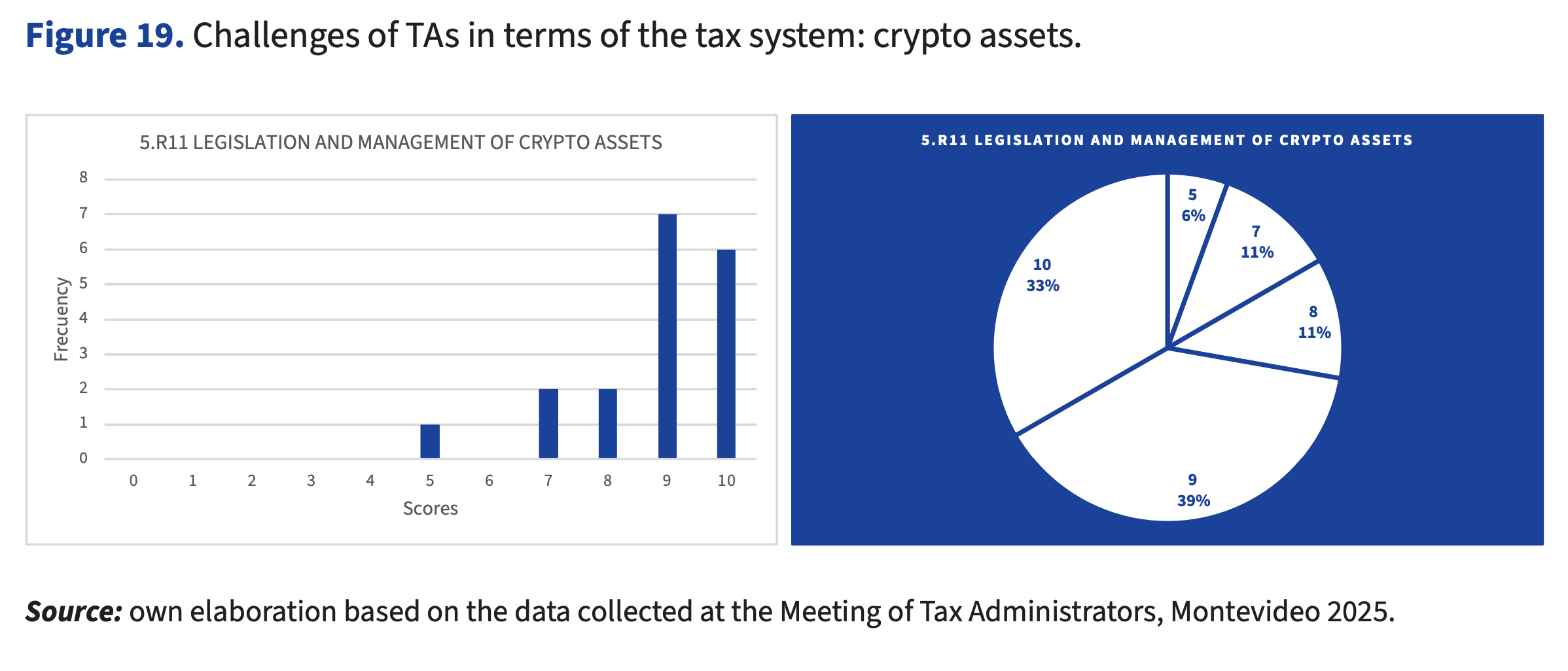

At the top are the challenges of the new digital economy, headed by how to deal with the taxation of crypto-assets, their legislation, and the adaptation of management to their special characteristics, with a high average score (8.8) and a high degree of consensus (Graph 19).

At the bottom of the list appears the challenge of facing the requirements of developing a global minimum tax (derived from international standards, although with a limited impact on collection in many cases) with an average score of 6.2 but with a high dispersion in valuations, which shows that, although for some administrations it is a top-order issue (five administrations, 28%, give it the maximum score), for others it is not among the most relevant challenges (seven administrations, 38%, score it below five).

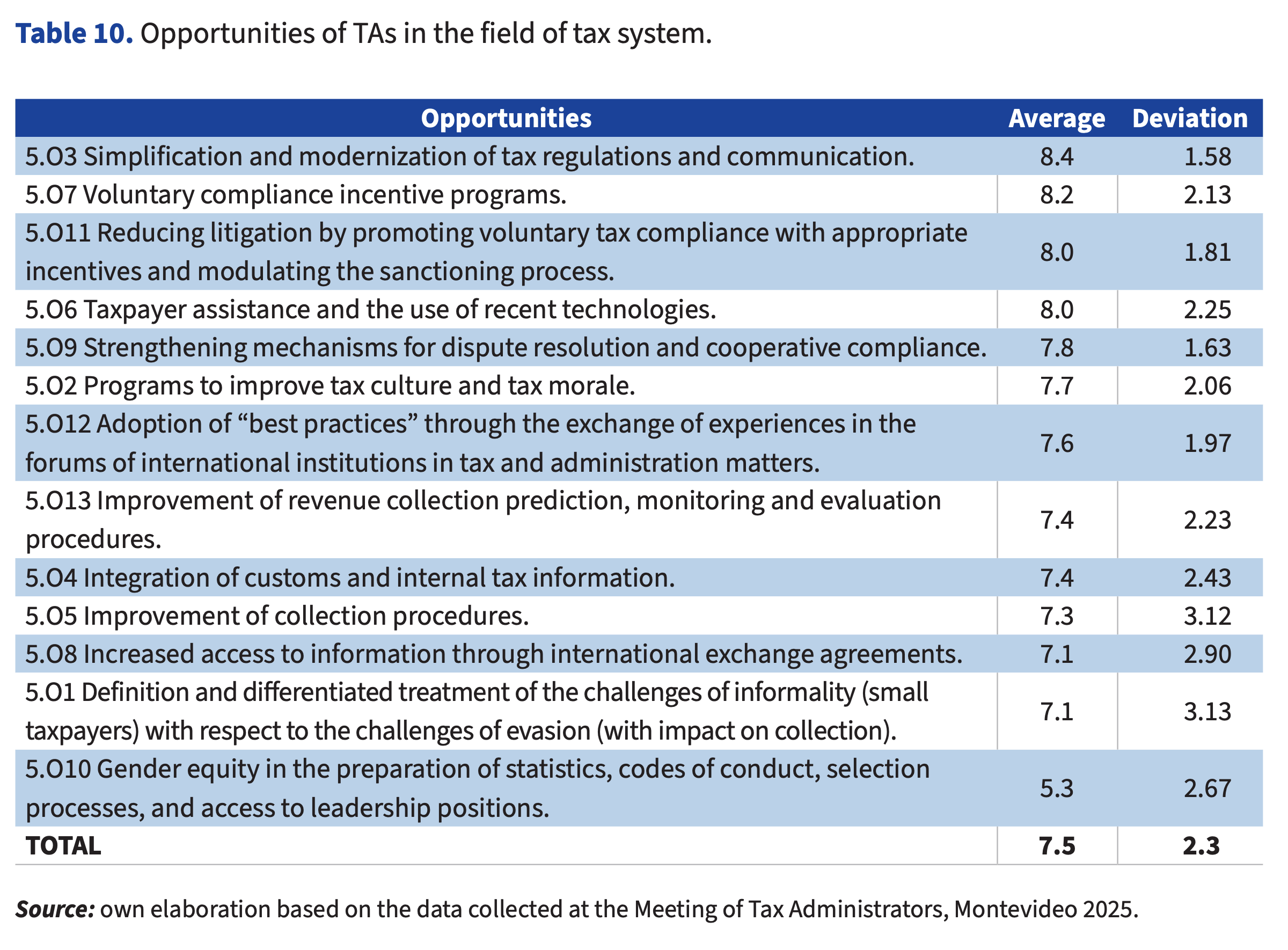

As for the opportunities in this area (Table 10; average 7.5; deviation 2.3) we find the following in order of scoring: simplification and modernization of tax regulations and communication; incentives for voluntary compliance; reduction of litigation and promotion of voluntary compliance; assistance to the taxpayer and use of new technologies; mechanisms for dispute resolution and cooperative compliance; improvement of tax culture and fiscal morality; adoption of “best practices” through the exchange of experiences in international institutional forums; forecasting, monitoring, and evaluation of revenue collection; integration of customs and internal tax information; collection procedures; international information exchange agreements; challenges of informality (small taxpayers) versus challenges of evasion (with an impact on collection); gender equality.

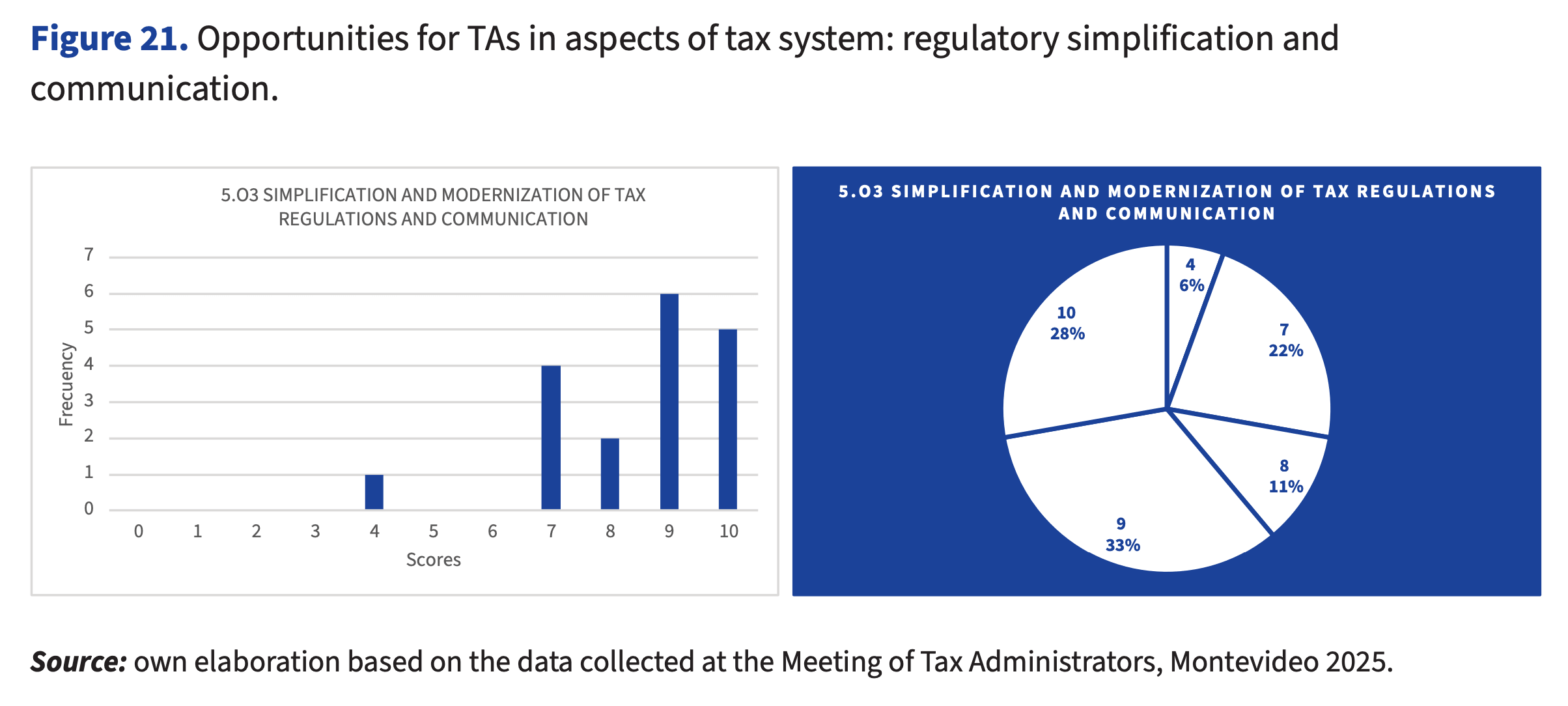

It is evident that the tax authorities’ approach to the tax system is based on promoting the paradigm of voluntary compliance. by utilizing the tools at their disposal, the simplification of tax regulations and communication is topping the list of opportunities, scoring 8.4 and enjoying a high degree of consensus (Figure 21).

The list of areas of opportunity for administrations concludes with their potential contribution to gender equity policies (in aspects such as the preparation of statistics, codes of conduct, recruitment processes, and access to leadership positions) with an average score of 5.3 and widely varying individual votes.

With this entry in CIATBlog, we conclude our review of the 120 challenges and opportunities identified at the Meeting. This significant sample represents twenty Tax Administrations -practically fifty percent of CIAT’s member countries across three continents, and the essential contribution of five international organizations and specialized institutions. This result is the product of an innovative methodology and the dedication of all participants, who are the true authors of this publication.

The discussion highlighted and identified key areas such as the adequate human talent attraction and retention, innovative new technologies, and the use of artificial intelligence for the best use of information and risk management, adaptation to the new digital economy, the modernization of institutional management, the facilitation of voluntary compliance or the potential advantages of international cooperation. While they show clear areas of consensus, the heterogeneity of each administration’s circumstances requires continued individualized attention.[1]

It is evident that the tax authorities’ approach to the tax system is based on promoting the paradigm of voluntary compliance. by utilizing the tools at their disposal, the simplification of tax regulations and communication is topping the list of opportunities, scoring 8.4 and enjoying a high degree of consensus (Figure 21).

References:

[1] In the publication Challenges and Opportunities of Tax Administrations, available with free access at the CIAT website, you can consult the publications, databases, technical assistance, software applications and training programs developed to meet these challenges and encourage the use of opportunities.

2,650 total views, 1 views today